Behavioral Accounting - Cognitive Failures and Judgment Bias in the Audit Suite

by Divya

4/15/20264 min read

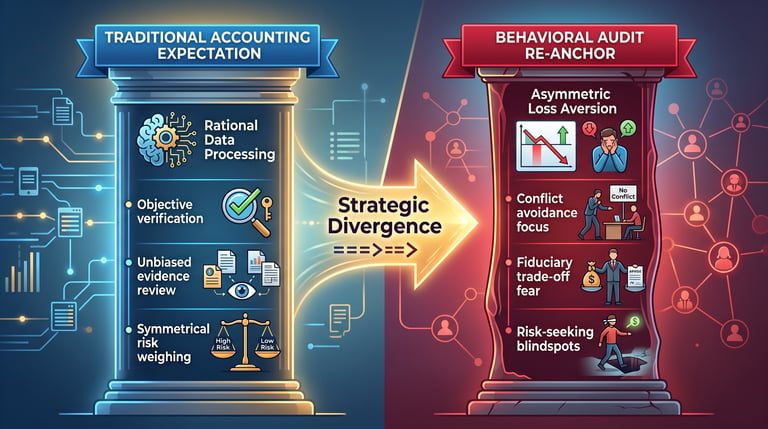

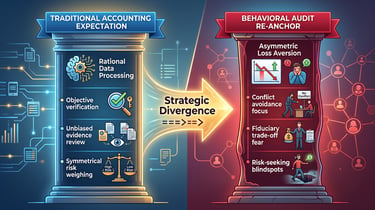

Financial auditing is traditionally evaluated through the lens of structural accounting rules and regulatory compliance. However, modern behavioral accounting research recognizes that financial statement integrity is heavily dependent on cognitive psychology. When corporate auditors evaluate highly subjective Critical Audit Matters (CAMs) such as goodwill impairment, fair value asset valuations, and complex legal provisions, they do not operate as perfectly rational data processors. Instead, auditors are vulnerable to systematic judgment biases that compromise professional skepticism. Grounded in Daniel Kahneman and Amos Tversky’s Judgment and Decision-Making (JDM) research, this briefing deconstructs how cognitive failures weaken the external defense layer of corporate governance.

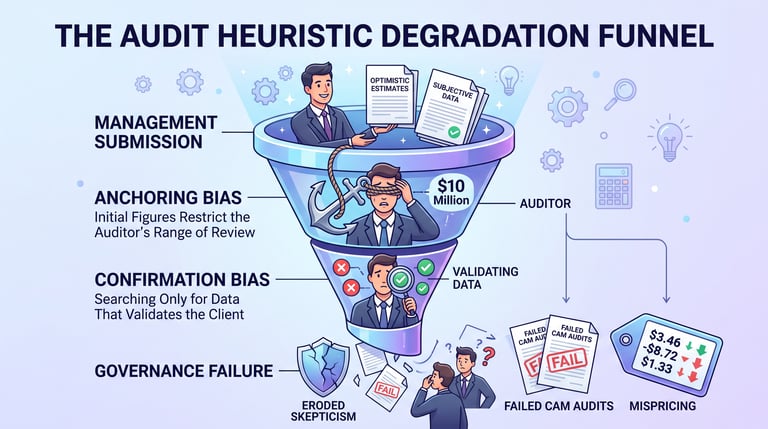

. The Anchoring Mechanism: Management Estimates as Psychological Anchors

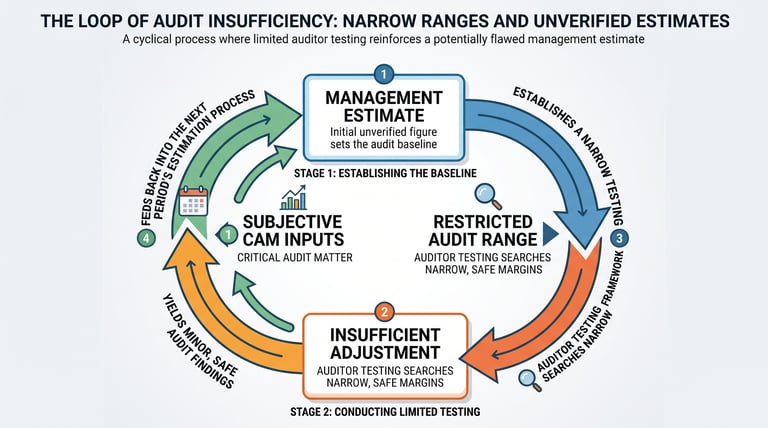

The fundamental breakdown of professional skepticism during complex asset valuations is driven by Anchoring Bias. This cognitive failure occurs when an individual relies too heavily on the first piece of information received when making subsequent decisions.

In a standard corporate audit, management presents its own internal, often highly optimistic valuation estimates for long-term intangible assets or complex financial instruments. Under JDM theory, this client-provided figure serves as a powerful psychological anchor.

Even a highly trained, experienced auditor who intends to challenge the figures will naturally structure their testing boundaries around that initial baseline. Instead of building an independent, objective valuation model from scratch, the audit team conducts narrow, safe adjustments, failing to look for structural mispricing that could exist outside those restricted margins.

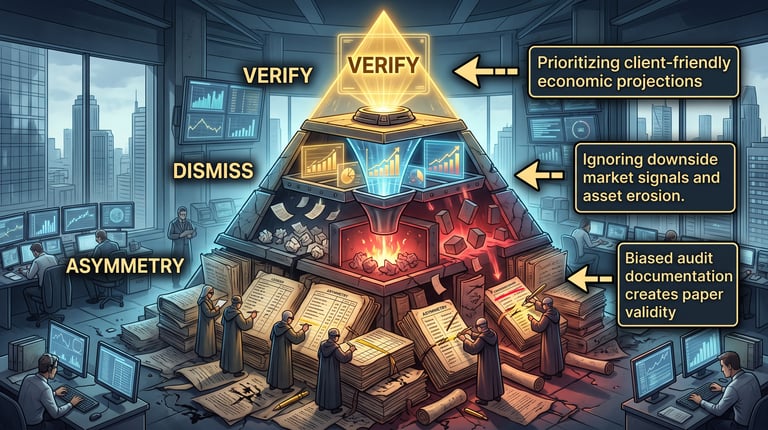

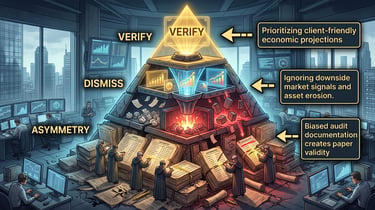

2. Confirmation Bias: The Asymmetric Search for Verification

Once an auditor is anchored to management's baseline valuation, cognitive friction is amplified by Confirmation Bias. This is the psychological tendency to search for, interpret, and prioritize data that supports pre-existing beliefs or choices, while completely ignoring conflicting evidence.

When evaluating a high-risk Critical Audit Matter (CAM), an auditor must actively seek out disconfirming evidence to test management's assumptions. However, due to confirmation bias, audit teams frequently fall into an asymmetric search pattern:

Biased Data Sourcing: Auditors over-index on internal client documents, upbeat industry reports, and management statements that justify the current asset valuation.

Dismissing Downside Signals: Conflicting external data points such as declining competitor stock performance, asset obsolescence indicators, or shifts in consumer behavior are frequently downplayed or rationalized away as temporary market anomalies.

Flawed Documentation: The resulting audit workpapers showcase an asymmetric collection of supporting evidence, creating a false paper trail of thorough testing while hiding systemic valuation risks from the public markets.

3. Financial Asymmetry: Applying Prospect Theory to Audit Choices

Kahneman and Tversky’s Prospect Theory provides a valuable framework for understanding why auditors struggle to push back against client misstatements. The theory demonstrates that human choices are asymmetrical: individuals are naturally risk-averse when facing potential gains, but become highly risk-seeking when trying to avoid certain losses.

In corporate auditing, this psychological loss aversion creates a dangerous dynamic:

The Cost of Confrontation: Forcing a client to restate their earnings or record a massive asset write-down triggers immediate, painful corporate losses, including damaged client-partner relationships, fee disputes, and potential account termination.

The Risk-Seeking Blindspot: Faced with the certain, immediate loss of a major corporate client versus the deferred, statistical probability of a future regulatory fine or shareholder lawsuit, the auditor's psychological framing shifts. They become risk-seeking, choosing to tolerate aggressive management estimates and hoping the valuation errors are never exposed by outside watchdogs.

4. Executive De-Biasing Protocols: Restructuring Audit Suite Choice Architecture

To protect professional skepticism from cognitive failure, corporate boards and audit committees must implement systematic de-biasing protocols that alter the underlying choice architecture of the audit suite:

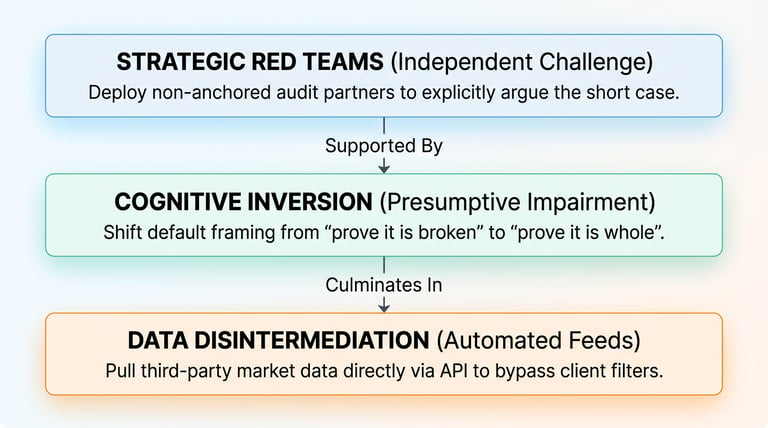

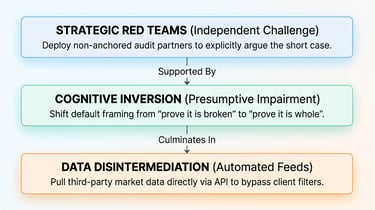

Deploy Independent Red Teams: Introduce a mandatory secondary review process led by a rotating audit partner who has zero direct contact with client management. This review partner must act as a "Red Team," explicitly attempting to dismantle the audit team's conclusions. Because this partner is not psychologically anchored to the client's initial figures, they can evaluate the asset valuation with complete objectivity.

Invert the Cognitive Framing: Shift the baseline operational question for complex CAM evaluations. Instead of asking audit teams to find evidence that proves an asset is impaired, change the mandatory default question to: "If this asset had to be liquidated tomorrow morning, prove with 100% external data that it is worth the value stated on the balance sheet." Inverting the framing neutralizes confirmation bias by forcing auditors to search for disconfirming information.

Automate External Data Feeds: Prevent auditors from relying exclusively on client-provided spreadsheets. Audit firms should mandate the use of automated, third-party data analytics platforms that pull macroeconomic indicators, commodity prices, and competitor valuation benchmarks directly into the audit software via APIs. Bypassing client-provided data filters ensures that auditors begin their analysis with an unanchored, objective market baseline.

Contact

Questions? Reach out anytime.

© 2025 BizSphere. All rights reserved.