Behavioral Traps in the Audit Suite and the Cognitive Architecture of the Enron Accounting Collapse

by Divya

4/16/20264 min read

The collapse of Enron Corporation in 2001 remains an archetypal landmark case study in structural and ethical corporate failure. However, academic behavioral accounting literature reveals that Enron’s systemic collapse was not merely a product of malicious intent; it was fundamentally accelerated by severe, unmanaged cognitive biases within its external auditor suite at Arthur Andersen.

Arthur Andersen, then one of the elite "Big Five" global accounting firms, failed to maintain professional skepticism because its senior leadership team fell victim to psychological anchoring, severe confirmation bias, and the catastrophic loss-aversion dynamics predicted by Daniel Kahneman and Amos Tversky’s Prospect Theory.

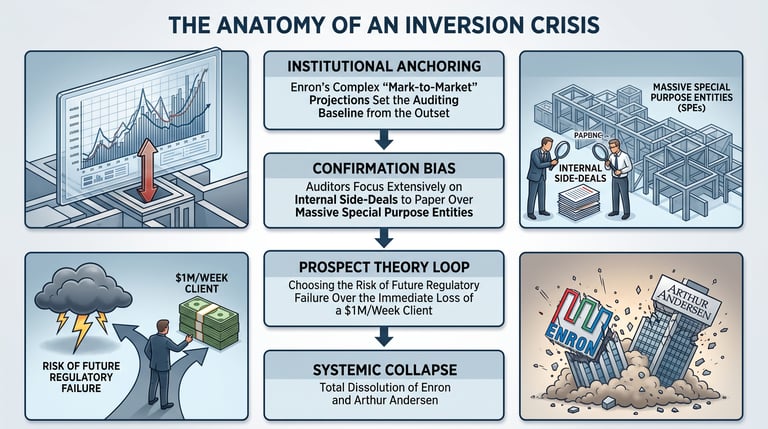

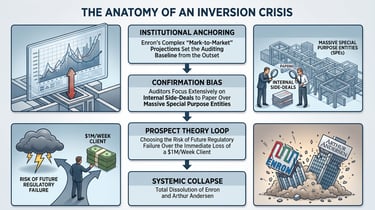

1. The Anchoring Mechanism: Mark-to-Market Schemes as Cognitive Anchors

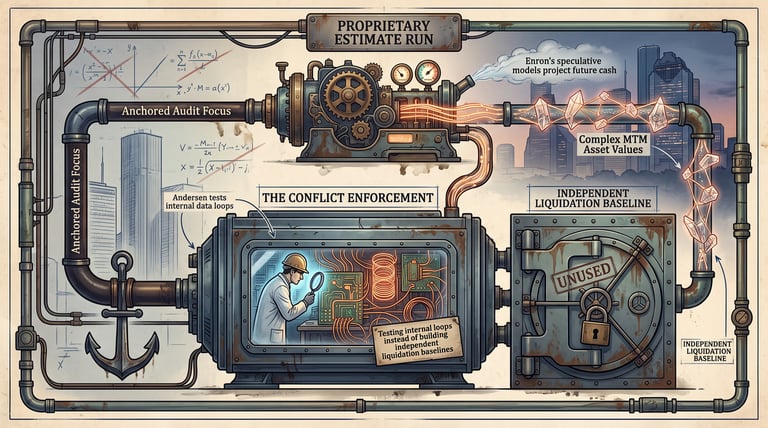

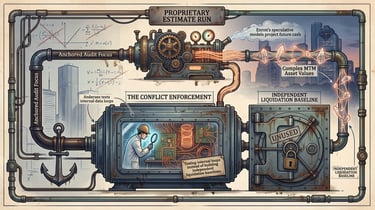

The root of Arthur Andersen’s cognitive breakdown lay in Enron’s aggressive deployment of Mark-to-Market (MTM) accounting for long-term, highly speculative energy contracts. MTM allowed Enron to estimate the future net present value of a 20-year energy project and book those hypothetical future profits on the day the contract was signed.

Under Judgment and Decision-Making (JDM) theory, these complex, proprietary mathematical models served as a powerful psychological anchor for the audit partners. Instead of building an independent, conservative liquidation model from scratch, Arthur Andersen’s audit teams accepted Enron’s initial projected figures as their analytical baseline.

They focused their subsequent testing entirely within narrow, safe adjustments around Enron’s models, validating the internal mathematics rather than questioning whether the underlying future revenue streams were entirely fictional.

2. Confirmation Bias and the Deception of Special Purpose Entities

Once Arthur Andersen’s audit suite was anchored to Enron’s stellar revenue growth projections, cognitive friction was amplified by an intense confirmation bias. To keep its stock price climbing, Enron began shifting billions of dollars of bad debt and toxic assets off its balance sheet into hundreds of shell companies, known as Special Purpose Entities (SPEs), such as Chewco and LJM.

To validate these fraudulent accounting structures, Arthur Andersen’s teams engaged in an asymmetric search for data:

Focusing on Paper Legality: The auditors meticulously reviewed internal legal documents and management representations that asserted the SPEs met the thin 3% outside equity requirement needed to remain un-consolidated.

Ignoring Real Cash Flows: The audit suite completely ignored critical downside warning signs, including the reality that these shell companies were backed entirely by Enron’s own stock, creating an existential loop of financial risk.

Suppressing Internal Warnings: When a senior Andersen risk partner, Carl Bass, voiced concerns about the aggressive nature of these transactions, the anchored engagement partners successfully lobbied Enron’s request to have Bass removed from his oversight role, actively eliminating disconfirming evidence to preserve their biased perspective.

3. Loss Aversion and the Collapse of Arthur Andersen

The ultimate downfall of the audit suite can be mapped through Prospect Theory. Kahneman and Tversky demonstrated that individuals are risk-averse when dealing with gains but become highly risk-seeking when trying to avoid a certain loss.

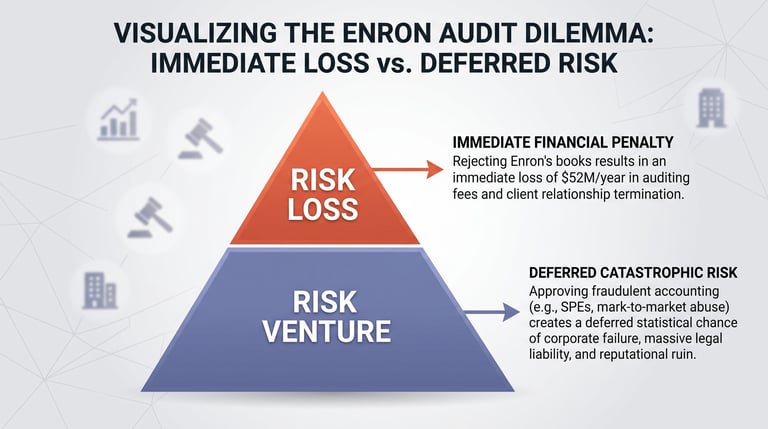

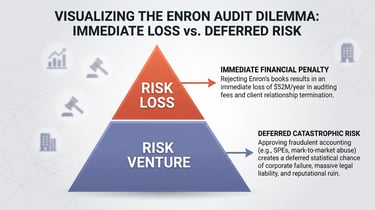

By 2000, Enron had become Arthur Andersen’s most lucrative global account, generating over $1 million per week in combined auditing and consulting fees.

This massive financial relationship inverted the risk calculus for Andersen’s leadership:

The Immediate Loss: If the audit partners maintained rigid professional skepticism and forced Enron to consolidate its toxic SPE debts, they faced an absolute, immediate loss: Enron would terminate the relationship, destroying the partners' careers and severely damaging the firm’s revenues.

The Risk-Seeking Venture: Faced with the certain loss of a $52 million annual contract versus the deferred, statistical probability of future regulatory failure, the partners chose to look the other way. They approved the distorted balance sheets, betting that Enron’s financial engineering would keep the company afloat indefinitely.

The Strategic Governance Conclusion

When Enron’s liquidity finally collapsed under the weight of its unrecorded debts in late 2001, the systemic fallout completely destroyed both firms. Arthur Andersen was convicted of obstruction of justice for shredding tons of audit documents in a desperate attempt to cover up its cognitive failures, leading to the rapid dissolution of the century-old firm and reducing the "Big Five" global accounting elite down to the "Big Four."

For future corporate executives, the Enron-Andersen collapse proves that a firm's internal controls are completely useless if its external defense layer is compromised by behavioral biases. True corporate governance requires building independent choice architectures that actively disrupt cognitive anchoring and prevent financial conflicts of interest from destroying professional skepticism.

Contact

Questions? Reach out anytime.

© 2025 BizSphere. All rights reserved.