Case Study Analysis: Systemic Failure and the Miscalculation of Risk Tolerance

by Divya

4/9/20264 min read

Corporate history highlights that catastrophic organizational failure rarely stems from a single, isolated event. Instead, systemic collapse is typically the result of senior leadership miscalculating the firm's risk tolerance, over-engineering financial returns, and ignoring early warning signs within the operational landscape. For future chief executives and risk directors, analyzing real-world operational breakdowns provides a clear warning on the dangers of decoupling aggressive growth metrics from rigorous risk-governance frameworks.

The collapse of Carillion plc in January 2018, a British multinational construction, facilities management, and defense services giant employing over 43,000 global workers—stands as a classic case study in risk miscalculation. Carillion's board of directors continually expanded into high-risk, low-margin, fixed-price construction contracts while simultaneously tolerating extreme financial leverage. When multi-million dollar operational bottlenecks occurred across its primary projects, the firm lacked the financial cushion to absorb the losses, triggering an immediate and catastrophic corporate insolvency.

The Strategic Alignment Failure: Mismanaging the 4 T’s

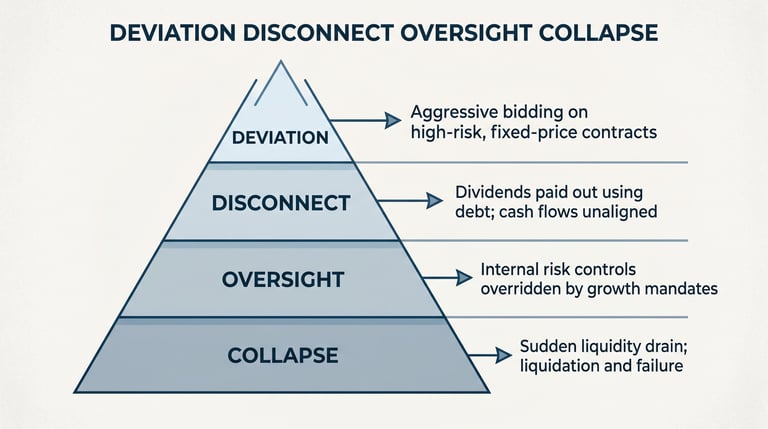

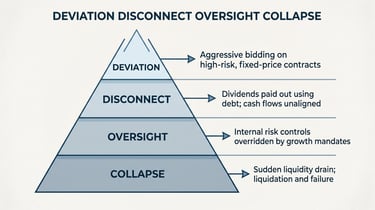

Carillion’s leadership committed a fatal error by choosing to Tolerate structural operational risks that should have been aggressively Treated or completely Terminated.

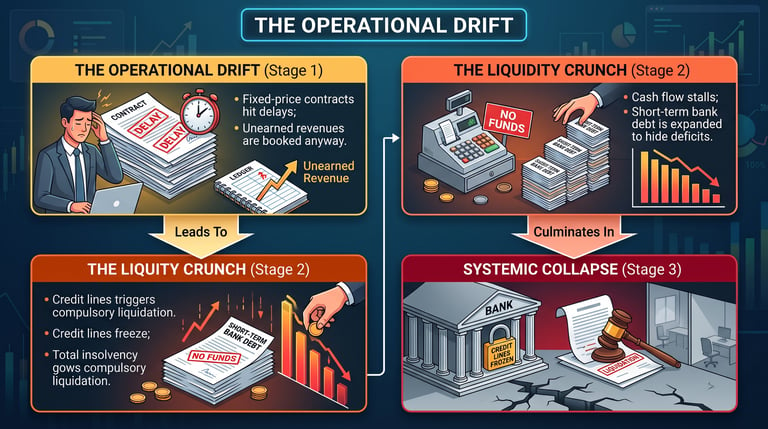

The multinational specialized in securing public-private partnership (PPP) mega-contracts by aggressively underbidding competitors. To win these bids, management accepted fixed-price terms, meaning Carillion assumed 100% of the financial liability for any future cost overruns, delays, or material price inflation.

In terms of risk strategy, management viewed these unpredictable, multi-year operational variables as routine risks that could be comfortably tolerated. In reality, the complex nature of mega-scale engineering projects meant that price changes and site delays were highly probable events with severe financial impacts. By failing to Treat these risks through contractual price-escalation clauses or Transfer them via specialized joint-venture partnerships, the board exposed the firm's entire balance sheet to extreme operational volatility.

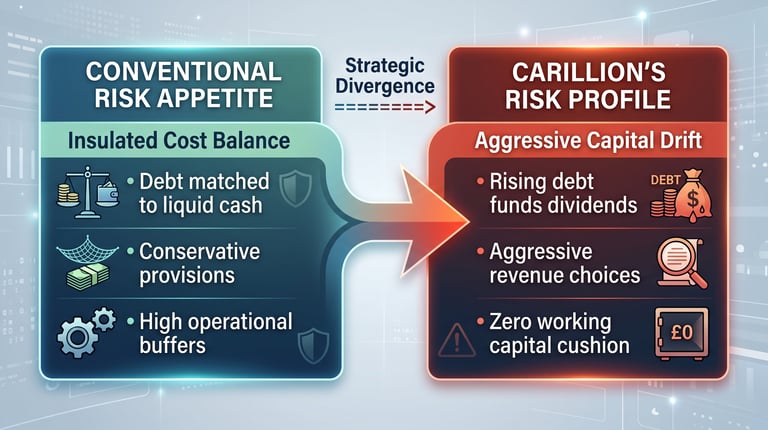

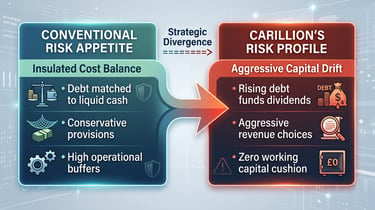

Aggressive Revenue Recognition: Leadership utilized loose accounting definitions to record unearned, disputed revenues from broken contracts as booked profits long before any cash was actually collected.

Debt-Funded Dividends: To maintain a positive image for investors, the board increased dividend payouts every single year, effectively using new debt to pay out cash to shareholders while the underlying business was actively draining cash.

Supply Chain Financing Abuse: Carillion forced its subcontractors to accept extended 120-day payment terms unless they took a financial discount through a bank-led early payment scheme. This allowed Carillion to reclassify its rising trade payables as bank debt, masking its true reliance on short-term credit to fund daily operations.

This complete breakdown of the internal capital filter meant that while the company's public financial statements reported steady profits, the firm's actual liquidity was completely exhausted, leaving it with zero working capital to survive a sudden market shift.

The Anatomy of Systemic Collapse

The structural fragility of the firm became obvious when three major international projects hit simultaneous delays. Carillion lacked the cash reserves to pay its subcontractors, causing work on its primary construction sites to ground to an immediate halt.

When the board attempted to secure an emergency financial rescue package, the capital markets refused to extend further credit due to the firm's high debt load and unreliable financial reporting. With billions in liabilities and a sudden freeze on its credit lines, the firm collapsed into compulsory liquidation in January 2018. The failure disrupted critical public infrastructure projects, cost thousands of jobs, and forced the government to step in to secure essential services, demonstrating the massive ripple effects when a major corporate infrastructure provider fails.

Key Takeaways for Future Executives

The systemic failure of Carillion offers three critical lessons for modern corporate governance:

Never Conflate Revenue with Liquidity: High revenue growth and a massive project pipeline mean nothing if the underlying contracts drain cash. Executives must judge business health based on cash generation rather than paper accounting profits.

Align Risk Appetite with Contractual Reality: If a firm operates in a low-margin sector, it cannot afford to tolerate high-impact risks. High operational uncertainty requires strict contractual limits, higher profit margins, and robust capital buffers.

Independent Board Oversight Is Vital: A primary reason for the collapse was a corporate culture that discouraged internal dissent, allowing executive growth mandates to override routine risk controls. Boards must ensure that risk officers possess the independent authority to challenge aggressive commercial growth assumptions before they expose the firm to systemic harm.

Explore More Business Articles

Contact

Questions? Reach out anytime.

© 2025 BizSphere. All rights reserved.