Corporate Governance and Allocation Decisions in Capital Budgeting

by Divya

4/7/20264 min read

Capital budgeting represents the ultimate deployment of corporate strategy. For future chief executive officers and financial directors, evaluating long-term projects is not a routine accounting task; it is the primary mechanism through which a firm commits capital to acquire long-lived assets, expand production capabilities, and secure sustainable competitive advantages. Because capital budgeting choices involve massive upfront cash outflows and highly uncertain multi-year return horizons, these decisions permanently dictate an enterprise's structural cost growth, strategic direction, and baseline corporate valuation.

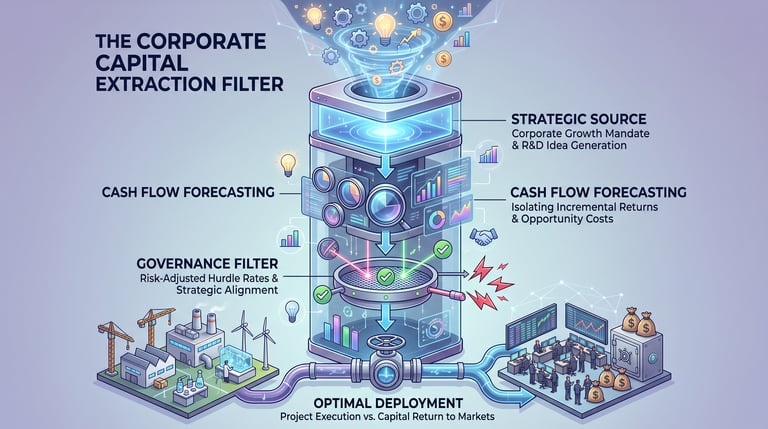

1. Isolating the Economic Cash Stream: Incremental Capital Allocation

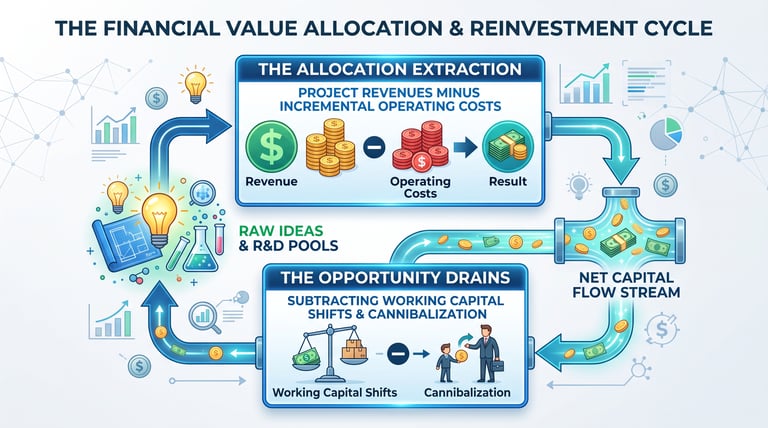

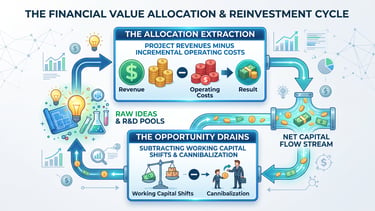

The foundational challenge in capital budgeting is the accurate projection of a project’s future cash flows. Corporate executives must maintain a sharp distinction between accounting profits and economic cash flows. Accounting net income includes non-cash expenses like depreciation and amortization, which distort the real timing of capital inflows and outflows.

To evaluate a project accurately, financial teams isolate the incremental cash flows, the net change in a corporation’s total cash flows that occurs as a direct consequence of accepting the project.

Isolating these cash flows requires corporate teams to adhere to three rigid principles:

The Irrelevance of Sunk Costs: Capital spent in the past on research, development, or market testing cannot be recovered and must be entirely ignored. Decisions should be forward-looking, based strictly on future capital requirements and returns.

Accounting for Opportunity Costs: If a project requires utilizing assets the firm already owns such as vacant corporate land or an idle manufacturing plant the market value of those assets if sold or leased must be charged against the project as a real cash cost.

Erosion and Cannibalization: When a company introduces a new product that takes sales away from its existing product lines, this revenue erosion must be treated as a negative cash flow. Conversely, positive side effects, where a new project boosts sales in an existing division, must be credited to the project.

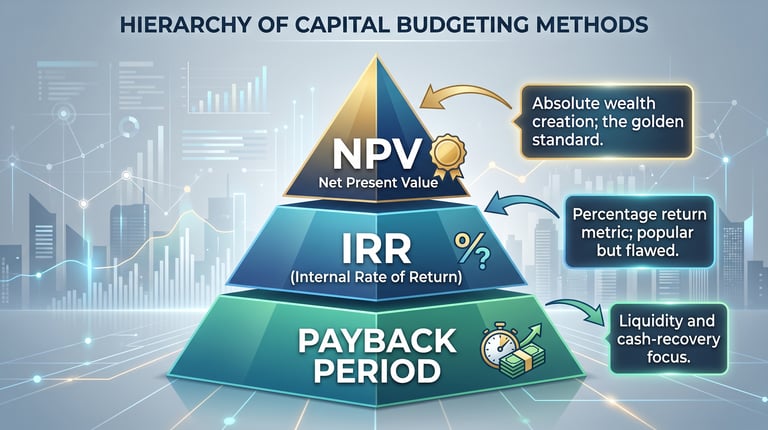

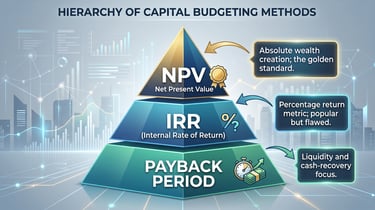

2. The Strategic Evaluation Toolkit: Non-Mathematical Comparison

To filter through competing corporate investments, executives rely on several standard evaluation frameworks. Each tool approaches the balance between time, risk, and capital recovery from a different strategic angle:

Net Present Value (NPV): Considered the gold standard of financial decision-making. NPV measures the absolute wealth created for shareholders by discounting all expected future cash inflows and outflows to the present day using the company's cost of capital. If the present value of inflows outpaces the initial capital cost, the project creates economic value.

Internal Rate of Return (IRR): Measures the expected percentage return on an investment. IRR is the specific return rate that balances a project's future cash inflows with its upfront costs. While executives prefer discussing projects in terms of percentage returns, IRR suffers from structural flaws. It assumes all intermediate cash flows can be reinvested at that same high rate, which can lead to distorted conclusions when comparing projects of different sizes or timeframes.

The Payback Period: A simple liquidity metric that measures how many years a company must wait to fully recover its initial cash investment. While it ignores the time value of money and cash flows generated after the break-even point, it remains popular as a risk-assessment tool in volatile markets where rapid capital recovery is necessary to prevent corporate insolvency.

3. Capital Rationing and Corporate Governance Strategy

In an ideal theoretical market, a corporation would fund every single project that displays a positive value-creation metric. In corporate reality, however, managers operate under capital rationing a strategic constraint where the firm sets a firm ceiling on the total capital budget available for deployment during a given fiscal period.

Capital rationing generally stems from two distinct forces:

Soft Rationing: Self-imposed budget ceilings designed by internal corporate leadership. Executives use soft rationing to prevent reckless, uncontrolled expansion, ensure management resources are not stretched too thin, and force business units to compete aggressively for capital, ensuring only the most highly profitable projects survive.

Hard Rationing: Driven by external capital market constraints. This occurs when a firm faces a restricted supply of external funds due to a low credit rating, a weak economy, or prohibitive equity issuance costs that prevent it from raising new debt or equity capital on reasonable terms.

Under tight capital constraints, corporate boards cannot rely on simple project rankings. They must evaluate how combinations of projects interact to maximize long-term corporate value, aligning each choice with the company's ultimate strategic focus.

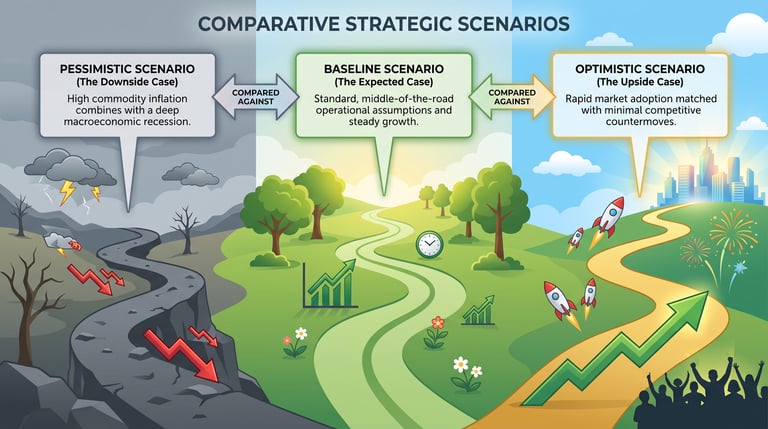

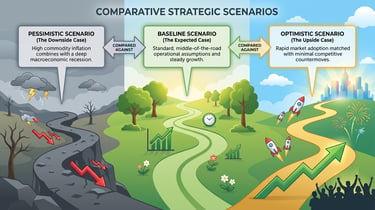

4. Advanced Risk Analysis: Scenario and Sensitivity Frameworks

Because capital budgeting estimates are based on multi-year projections, they are highly vulnerable to forecasting errors. Sophisticated corporate governance teams do not rely on a single, static set of numbers. Instead, they use advanced risk frameworks to stress-test projects before committing capital.

Scenario Analysis: Evaluating Systemic Shifts

Unlike sensitivity analysis, scenario analysis evaluates a coordinated change in several interconnected variables simultaneously. Management builds distinct operational scenarios to model potential real-world economic environments:

By analyzing these diverse scenarios, executive boards gain a complete view of a project's risk profile. This enables leadership to pass on high-risk projects that threaten corporate stability during a downturn, while aggressively funding resilient investments that strengthen the firm’s competitive moat regardless of broader market fluctuations.

Contact

Questions? Reach out anytime.

© 2025 BizSphere. All rights reserved.