How Behavioral Corporate Finance Biases and Executive Hubris Drive Catastrophic Valuation Errors

by Divya

3/27/20263 min read

The assumption that corporate managers and retail investors process information symmetrically, calculate risks objectively, and always make choices that maximize enterprise value is the foundation of standard MBA-level financial models. When you step out of the textbook and into real-world executive suites, however, you quickly discover that corporate finance is driven by human beings. Behavioral corporate finance explores how psychological biases, emotional traps, and cognitive blind spots cause seasoned executives to make catastrophic capital allocation errors, proving that understanding these psychological dynamics is just as critical to an advanced financial education as mastering a discounted cash flow spreadsheet.

The most destructive psychological force in corporate finance is executive overconfidence, which is best explained by the hubris hypothesis of corporate takeovers. Developed by financial economist Richard Roll, this theory illustrates why companies consistently pay too much money to acquire other businesses during mergers and acquisitions. In a perfectly rational market, an acquiring company should only buy a target firm if the transaction generates clear operational synergies. However, overconfident chief executive officers regularly suffer from an illusion of control, believing their personal management team can extract value from a target company where all previous owners failed.

When a corporate leader succumbs to hubris, they over-estimate future revenue growth and under-estimate integration costs. This psychological distortion causes them to pay an excessive premium price, which effectively transfers all potential wealth from the acquiring company's shareholders straight to the target firm's sellers, trapping the organization in a value-destruction loop.

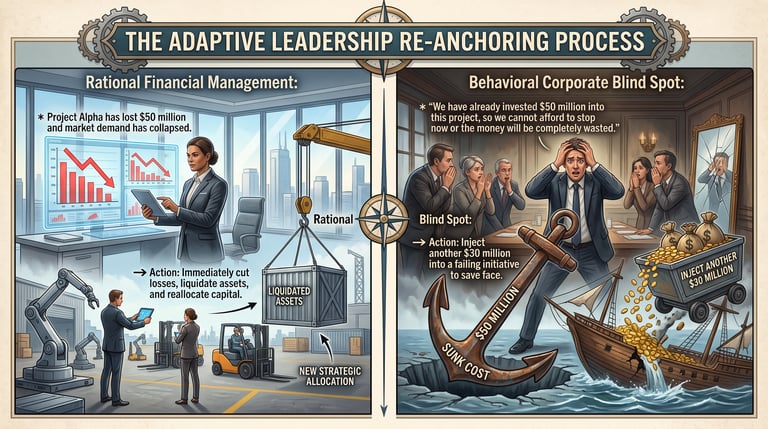

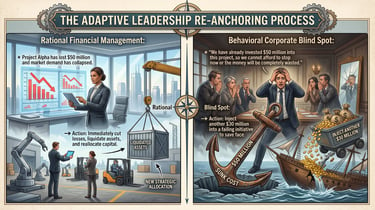

Another critical behavioral trap taught in top-tier corporate finance seminars is the escalation of commitment, driven by loss aversion and the sunk cost fallacy. According to prospect theory, human beings experience the pain of a financial loss twice as intensely as they experience the pleasure of an equivalent gain. In the boardroom, this manifests as an executive’s complete inability to admit that a major strategic project or capital investment has failed.

When an executive frames a project shutdown as a personal failure, they choose to pump more capital into a dying initiative. They do this hoping to break even, rather than cutting their losses and shifting those corporate resources to higher-yielding assets.

To understand how these cognitive distortions impact corporate budgeting, look at the systematic variance between an executive team's projected internal rate of return and the actual, realized post-implementation returns. The planning fallacy worsens as projects become more complex and unfamiliar. While routine infrastructure investments track closely to expectations, complex acquisitions and research and development programs show a severe performance gap because boardroom optimism routinely sidelines objective, data-driven historical realities.

To protect public corporations from these systemic psychological pitfalls, corporate governance directors use specific de-biasing frameworks designed to strip emotion out of financial engineering. One method is establishing an independent "devil's advocate" peer review unit. This team is tasked with intentionally finding vulnerabilities in a proposal's assumptions, stress-testing revenue growth projections, and highlighting hidden integration costs to counter executive confirmation bias.

Advanced organizations also practice project pre-mortems. Before a single dollar is deployed, the executive team gathers to imagine that the initiative has completely failed five years into the future. Writing down the hypothetical history of that catastrophe overrides corporate groupthink, making it psychologically safe for team members to flag structural risks early on. Finally, corporate treasuries enforce reference class forecasting, which forces divisions to anchor their financial models using actual, realized statistical data from a large pool of similar, completed historical projects, neutralizing local overoptimism.

For future financial leaders, the key takeaway is to beware of the synergy mirage. In the vast majority of corporate acquisitions, the projected operational synergies fail to materialize. Always value a target company based on its standalone cash flows, treating potential synergies as a speculative bonus. Furthermore, protect your firm from the escalation of commitment by defining strict, non-negotiable financial performance triggers before a project launches. If a project hits a specific milestone flag without meeting its goals, kill it immediately regardless of how much capital has already been spent. Finally, audit your corporate culture regularly, because if your company rewards blind optimism and punishes managers who bring bad news to light, your internal financial data will always be compromised by psychological bias.

Contact

Questions? Reach out anytime.

© 2025 BizSphere. All rights reserved.