How Financial Accounting Standardized Reporting Dictates Capital Allocation Mechanics in Global Markets

by Divya

3/26/20264 min read

For MBA students and finance professionals, global capital markets often resemble a high-frequency digital battlefield. Trillions of dollars shift across borders every second, driven by algorithms, macroeconomic signals, and changing interest rates. But beneath this complex financial architecture sits a foundational layer that makes investment possible: Accounting.

Without a universal, standardized language to measure and verify corporate performance, capital markets would experience systemic collapse. Accounting isn't merely an administrative record-keeping task; it is the vital information engine that transforms raw economic data into trust, liquidity, and efficient capital allocation.

This masterclass explores how financial accounting serves as the structural backbone of capital markets, analyzes the economics of information asymmetry, and maps out how accounting metrics dictate the cost of corporate capital.

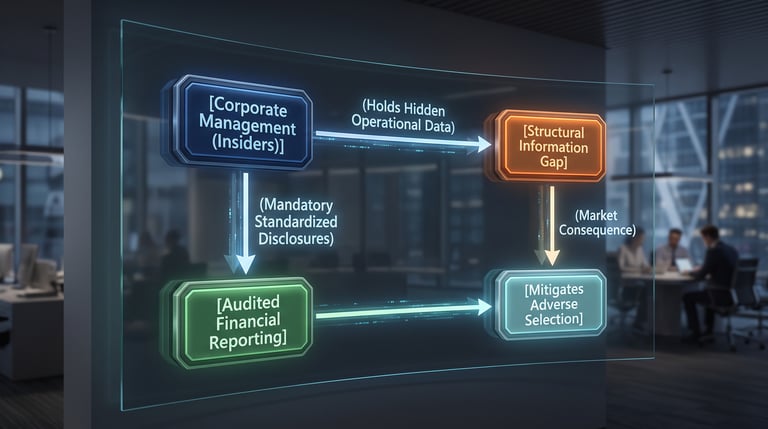

1. The Core Economic Framework: Mitigating Asymmetric Information

In corporate finance, the relationship between corporate managers and outside investors is governed by a fundamental hurdle known as The Principal-Agent Problem.

Corporate insiders (the agents) possess a deep, intimate understanding of a company’s operational health. Outside investors (the principals) are starved for information. This structural imbalance is known as Information Asymmetry.

Left uncorrected, information asymmetry triggers two distinct market failures:

Adverse Selection (Pre-Transaction): When buyers cannot differentiate between high-quality companies and low-quality "lemons," they lower the price they are willing to pay for all stocks. This drives healthy companies out of the public markets.

Moral Hazard (Post-Transaction): Once investors hand over their capital, they cannot easily monitor whether executives are deploying that money efficiently or consuming luxury corporate perks.

Standardized financial accounting governed by frameworks like US GAAP and IFRS,is the structural mechanism designed to clear this bottleneck. By forcing corporations to release audited, uniform, periodic financial statements (10-Ks and 10-Qs), accounting bridges the information gap, allowing investors to allocate capital with absolute confidence.

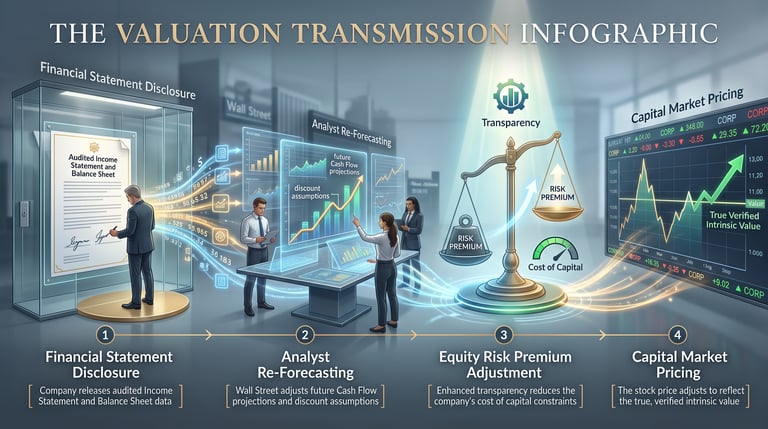

2. The Accounting Transmission Mechanism: From Ledger to Valuation Multiples

How exactly does a row in a general ledger translate into an equity price on the New York Stock Exchange? This dynamic occurs through a systematic transmission mechanism that impacts investor behavioral psychology and mathematical valuation metrics.

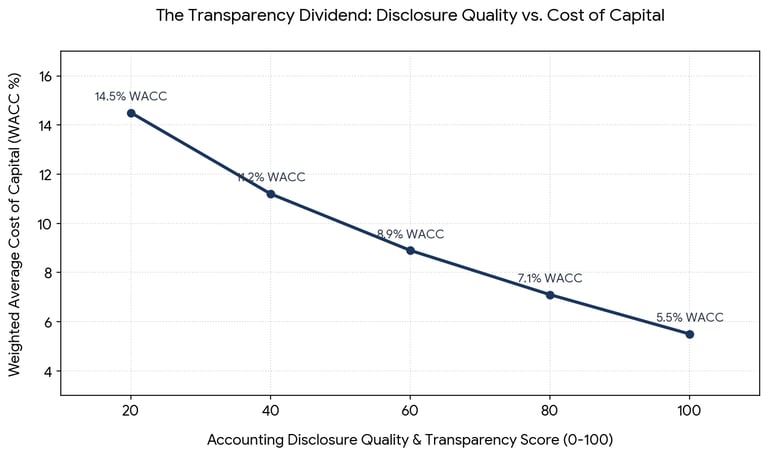

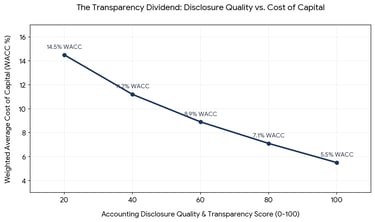

3. Visualizing the Impact: Information Quality vs. Cost of Capital

For corporate treasurers, accounting transparency is directly tied to cash optimization. When a corporation provides high-quality, transparent, and frequent accounting disclosures, it slashes its Cost of Capital (the interest rate it pays on debt and the return demanded by equity holders).

The following chart illustrates the inverse correlation between accounting disclosure quality scores and a firm's Weighted Average Cost of Capital (WACC):

When a firm moves from a low-transparency regime to an elite disclosure standard, its cost of capital drops dramatically. This occurs because investors no longer demand a high "information risk premium" to protect themselves against unexpected financial surprises.

4. Advanced Capital Market Frameworks for MBA Analysis

When analyzing accounting's role in capital markets during your corporate finance modules, anchor your research inside these three foundational corporate finance frameworks:

The Efficient Market Hypothesis (EMH)

Accounting disclosures serve as the fundamental fuel for market efficiency. Under the semi-strong form of EMH, public stock prices instantly adjust to incorporate all publicly available information. When an accounting team drops an unexpected earnings surprise in an SEC filing, the stock price recalibrates within milliseconds, proving that capital markets continuously ingest and process accounting data to refine asset pricing.

Quality of Earnings Analysis

Sophisticated asset managers look far past the headline net income figure to evaluate the underlying Quality of Earnings. This process involves assessing how closely a company’s paper accounting profits track its true cash generation:

Quality of Earnings Ratio = Operating Cash Flow ÷ Net Income.

If a company reports skyrocketing net income but flat or negative operating cash flow over multiple quarters, it signals aggressive revenue recognition policies, growing inventory bloat, or artificial accounting manipulation.

Earnings Management & Accrual Anomalies

Because accrual accounting relies on management estimates (such as depreciation schedules and bad debt allowances), executives occasionally engage in Earnings Management to smooth out volatile earnings patterns. MBA analysts utilize tools like the De擺o Model or the Modified Jones Model to isolate total accruals from non-discretionary cash flows, helping them flag potential accounting manipulation before it triggers a public corporate restatement.

Key Takeaways for Corporate Finance Scholars

Market makers widen their bid-ask spreads when they suspect a high concentration of inside information. Uniform accounting standards narrow these spreads, boosting market depth and liquidity.

Capital is highly risk-averse. Countries with weak, opaque, or corrupt national accounting standards experience severe capital flight, as global institutional funds avoid non-transparent regulatory frameworks.

Paper net income is an executive's estimate, but cash flow is an absolute economic fact. Always run a Quality of Earnings check to confirm that a company's stated accounting returns are backed by operational liquidity.

Explore More Business Articles

Contact

Questions? Reach out anytime.

© 2025 BizSphere. All rights reserved.