Navigating the Complex Friction Between Corporate Purpose and Public Market Primacy

by Divya

4/2/20265 min read

Danone SA, a multinational food-and-beverage giant headquartered in Paris, operates across more than 120 countries with a highly diversified product portfolio split into four primary business units: Specialized Nutrition (Early Life and Medical Nutrition), Essential Dairy and Plant-Based Products (featuring global brands like Activia, Oikos, and Silk), and Waters (such as Evian and Volvic). Historically, Danone has positioned health, nutrition, and environmental sustainability at the absolute center of its corporate strategy.

This dual commitment to economic success and social progress first articulated in 1972 by then-CEO Antoine Riboud as the "Dual Project" was radically accelerated under the leadership of Emmanuel Faber, who took over as CEO in 2014 and Chairman in 2017. Faber became a prominent global voice for stakeholder capitalism, steering the company toward aggressive environmental, social, and governance (ESG) targets. Under his stewardship, Danone achieved significant milestones, including becoming the first publicly listed French corporation to adopt the legal status of an Entreprise à Mission (purpose-driven company) in 2020. This legal designation officially amended Danone's corporate charter, binding the organization to social and environmental goals alongside its financial responsibilities to shareholders.

Despite these progressive structural achievements, Danone’s financial performance began lagging significantly behind its primary peer group, notably Nestlé and Unilever. The arrival of the COVID-19 pandemic exacerbated these vulnerabilities, depressing sales in the high-margin Waters division due to the closure of away-from-home hospitality channels, while commodity inflation squeezed operating margins. Recognizing stagnant stock performance, a drop in return on capital employed (ROCE), and operational inefficiencies, a group of activist investors led by London-based Bluebell Capital and US-based Artisan Partners acquired stakes in Danone. The activists initiated an aggressive campaign demanding structural restructuring, the separation of the CEO and Chairman roles, and a pivot back to margin maximization. This governance crisis culminated in March 2021, when the board of directors bowed to investor pressure and removed Emmanuel Faber from his positions, creating a pivotal landmark case regarding the viability of responsible capitalism in public equity markets.

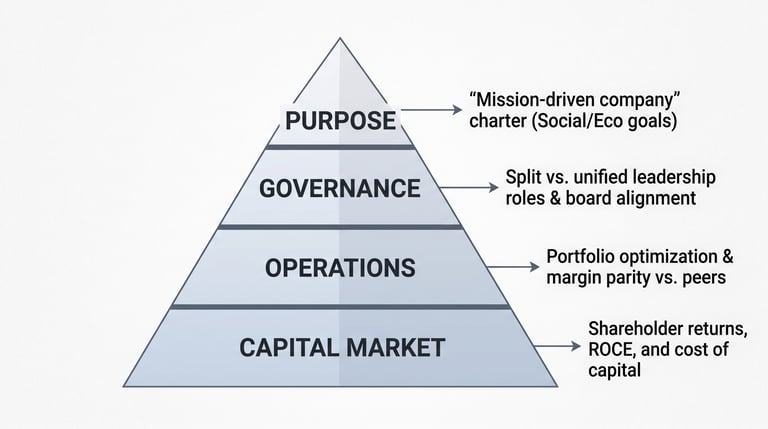

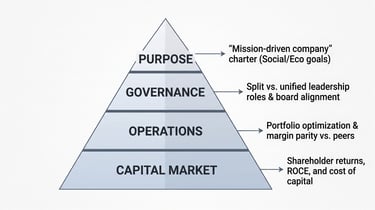

The Strategic Balance Matrix

To analyze the structural dynamics that led to this corporate crisis, we must look at how corporate strategy, capital allocation, and governance frameworks intersect.

Organizations that attempt to pursue transformative corporate sustainability must maintain balance across all levels of the Strategic Balance Matrix. If the foundational layer capital market performance and operational efficiency crumbles, the upper layers of progressive governance and overarching corporate purpose become structurally unsustainable, exposing the firm to activist intervention.

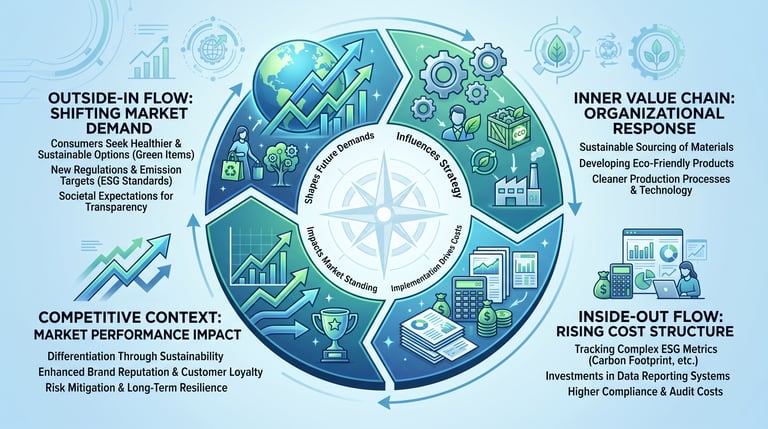

Outside-In vs. Inside-Out Dynamics in Danone’s Failure

Danone’s strategic friction can be effectively evaluated using the tension between outside-in and inside-out strategic alignment frameworks.

Faber executed an aggressive inside-out approach, redesigning the internal value chain to champion sustainability. He implemented internal carbon pricing, poured capital into regenerative agriculture partnerships with local dairy farmers, and pushed for expensive, sustainable packaging transformations.

However, this inside-out transformation failed to align cleanly with the outside-in competitive context. While consumers expressed a preference for healthy and sustainable alternatives, Danone’s complex operational structure could not convert those preferences into superior market premiums or profit margins that matched its competitors. At the same time, the outside-in pressures of the capital markets required strict cost control and consistent shareholder returns expectations that Danone's rising cost structure failed to meet.

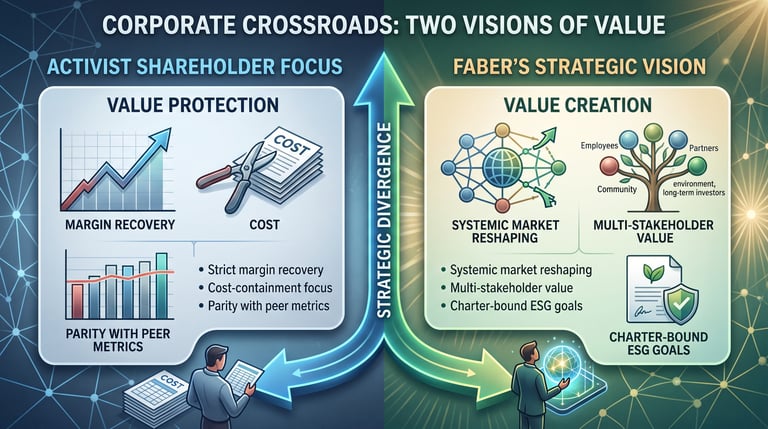

The Growth & Ambition Stage Continuum

The friction between Faber and the activist shareholders is fundamentally a clash of differing ambitions on the corporate sustainability maturity continuum.

Activist shareholders viewed the company through a value protection lens, arguing that Danone must first guarantee profit margins and secure competitive operational health before spending capital on experimental social goals. Conversely, Faber operated at a value creation stage, attempting to redefine the company’s purpose to reshape the wider food industry ecosystem, even if it meant tolerating lower near-term margins and higher execution risks.

Case Study Analysis: Formal Responses to Prompts

Question 1: In what ways could Emmanuel Faber and the Danone board have defended their strategy of pursuing a purpose beyond profit?

To defend a dual-purpose strategy against sophisticated activist investors, corporate leadership cannot rely on abstract ethical arguments. They must construct a defense rooted in financial economics, operational milestones, and strategic risk management. Faber and the board could have mounted a defense through three main mechanisms:

Direct Financial-ESG Integration (The Economic Case): Management should have framed their sustainability initiatives not as auxiliary cost centers, but as defensive investments to protect long-term value. For example, spending capital on regenerative agriculture should have been validated as a way to secure supply chain resilience against climate-driven crop failures and volatile dairy pricing. They needed to present data demonstrating that carbon reduction directly insulates the company from future European carbon taxes and regulatory penalties. By framing ESG as a risk-mitigation tool that lowers the company's long-term cost of capital, they could have spoken to investors in an economic language they understood.

Phased Operational Milestones and Margin Targets: A core vulnerability for Danone was that its financial underperformance coincided with its loudest public proclamations on stakeholder purpose, allowing activists to create a cause-and-effect narrative between the two. The board should have established a transparent framework where ESG commitments were rolled out in phases, strictly tied to achieving baseline operating margins. By ensuring that major sustainability investments were executed only when core operational KPIs met peer benchmarks, management could have neutralized the activist argument that purpose was an expensive distraction from profit.

Proactive Management of the Investor Base (Courting Patient Capital): A publicly traded firm cannot easily execute a long-term multi-stakeholder transformation if its shares are held primarily by short-term arbitrage and momentum funds. The board and executive leadership should have systematically reshaped Danone's equity base years prior to the crisis. By actively marketing to sovereign wealth funds, long-term pension systems, and green institutional funds that prioritize multi-decade risk mitigation over quarterly earnings beats, Danone could have built a protective wall of "patient capital" to insulate management from short-term public market volatility.

Question 2: Does the ousting of Emmanuel Faber indicate a shift away from Danone’s commitment to responsible capitalism?

The ousting of Emmanuel Faber does not indicate a systemic rejection of responsible capitalism or a retreat from Danone’s core ESG commitments. Instead, it highlights a structural lesson in corporate governance: stakeholder capitalism cannot exist without operational competence.

Retention of the Legal Charter (Entreprise à Mission): The most compelling structural proof that Danone did not abandon its commitment to responsible capitalism is that the activist investors did not attempt to dismantle or revoke Danone's legal status as an Entreprise à Mission. The corporate charter remains legally amended to require social and environmental governance. The activists did not object to the concept of corporate responsibility itself; they objected to poor financial execution, falling market share, and lagging returns relative to Nestlé and Unilever.

The Reality of Operational Interdependence: The case demonstrates that purpose and profit are not mutually exclusive, but completely co-dependent. A company requires strong financial margins to generate the excess capital needed to fund its progressive environmental and social missions. When a firm underperforms financially, it loses the market credibility required to defend its long-term strategy, inviting external intervention.

The Strategic Conclusion: Faber’s removal was an operational correction rather than an ideological shift. It reinforces that the baseline requirement of modern executive leadership is to run a highly competitive, financially disciplined business. Only by achieving operational excellence can a firm earn the strategic autonomy required to deliver on its broader commitments to society, the environment, and the global community.

Contact

Questions? Reach out anytime.

© 2025 BizSphere. All rights reserved.