The Financial Engineering of Debt: Strategic Frameworks for Corporate Bond Valuation

by Divya

4/6/20265 min read

Bond valuation is a fundamental tool for capital allocation, corporate financial engineering, and risk management. For future Chief Financial Officers and investment managers, a bond is more than a simple fixed-income security; it represents a legally binding, long-term contract governing the cost of debt capital. Evaluating these instruments requires a sophisticated understanding of discounted cash flow (DCF) mechanics, structural interest rate sensitivity, and market-driven risk premiums. Mastering bond valuation frameworks allows corporate leaders to optimize capital structures, timed debt issuances, and accurately assess the market’s perception of a firm's credit risk.

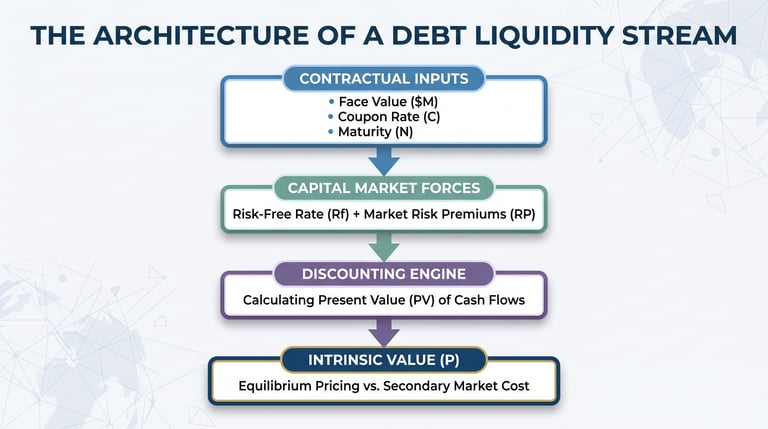

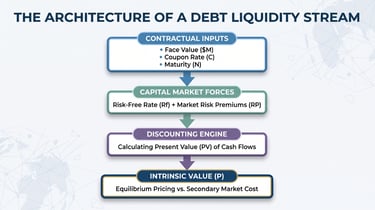

1. The Mathematical Foundation: Time Value of Money in Debt Pricing

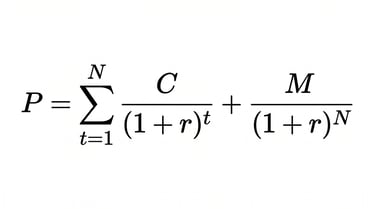

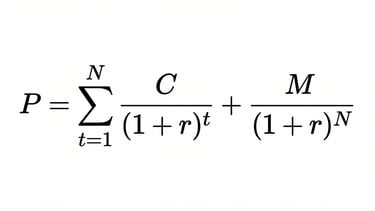

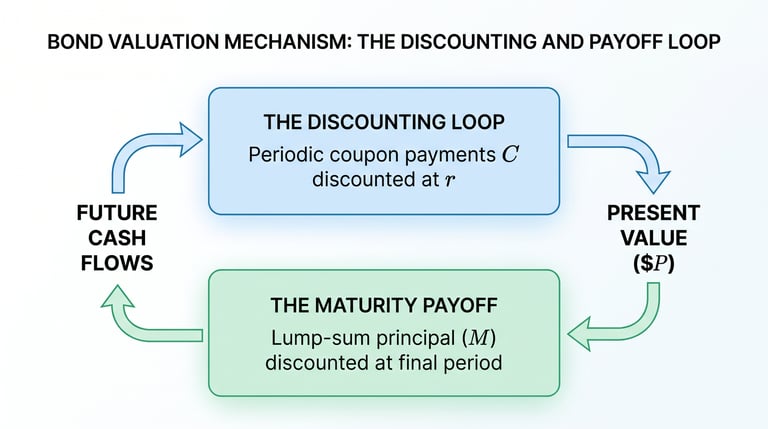

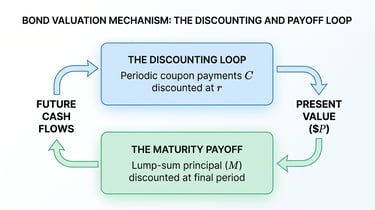

At its algorithmic core, the intrinsic value of a bond is calculated by discounting its future cash flows to the present day using the investor's required rate of return, or yield to maturity (YTM). These cash flows consist of a series of periodic coupon payments and a single lump-sum principal repayment at maturity.

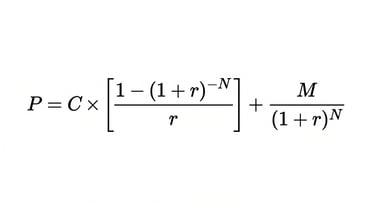

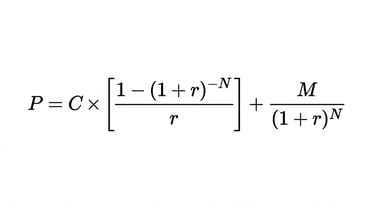

The universal valuation formula for a standard fixed-rate corporate bond is expressed as:

Alternatively, when using financial annuity notation for simplified computation, the formula is structured as:

Where:

P = The intrinsic value or market price of the corporate bond.

C = The periodic coupon payment, derived by multiplying the face value by the annual coupon rate (C = M × Coupon Rate / Periods per Year).

r = The periodic required rate of return, or Yield to Maturity (YTM).

N = The total number of compounding periods remaining until final maturity.

M = The par value, face value, or principal repayment amount of the bond (typically standardized at $1,000).

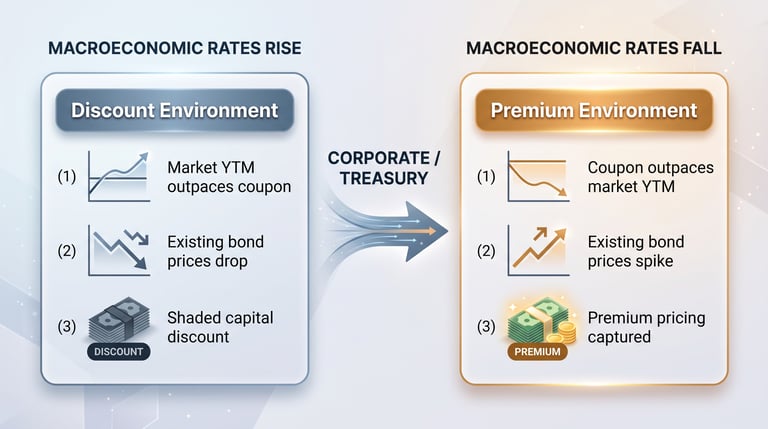

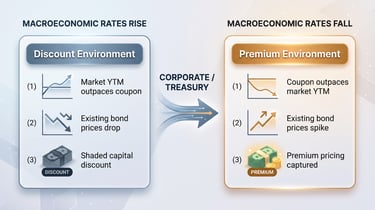

2. Market Dynamics: The Inverse Relationship Matrix

A critical operational reality for corporate treasurers is the fluid relationship between a bond’s fixed coupon rate and the market’s constantly changing required rate of return (YTM). Because a bond's contractual coupon payments remain locked at issuance, the secondary market price of the bond must fluctuate to align its total yield with prevailing macroeconomic interest rates.

This structural alignment creates three distinct pricing environments on the valuation continuum:

Premium Bonds (P > M): Occurs when a firm's coupon rate is higher than the current market interest rate. Because the bond pays above-market returns, investors bid up its price until its total yield matches the market average.

Par Bonds (P = M): Occurs when the coupon rate exactly equals the market’s required rate of return. The security trades at its face value.

Discount Bonds (P < M): Occurs when market interest rates rise above the bond’s fixed coupon rate. Because the bond's payouts are uncompetitive, its market price drops below par value to offer investors capital appreciation that offsets the lower coupon yields.

3. Structural Risk Management: Interest Rate Volatility and Duration

For investment managers and corporate CFOs, understanding how sensitive a debt portfolio is to interest rate shifts is critical for managing balance sheet risk. This sensitivity is dictated by two structural elements: time to maturity and coupon size.

The Maturity Effect: Long-Term Volatility

Long-term bonds experience significantly higher price volatility when interest rates shift compared to short-term bonds. This occurs because a larger portion of a long-term bond's total cash flow is locked far in the future, compounding the discounting effect over more periods.

The Strategic Risk: An unexpected increase in macroeconomic interest rates causes immediate capital losses for holders of long-term debt assets.

The Coupon Effect: Capital Concentration

Bonds with lower coupon rates are more sensitive to interest rate changes than high-coupon bonds. A low-coupon security backloads its total return, concentrating its cash flow in the final principal payment. Conversely, a high-coupon bond returns cash to investors faster, reducing its long-term exposure to interest rate shifts.

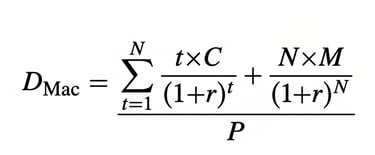

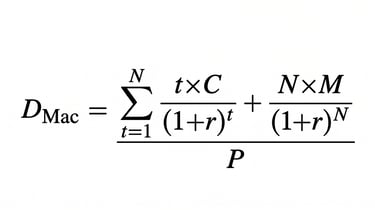

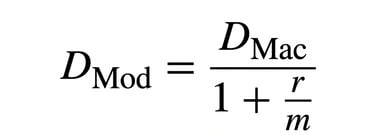

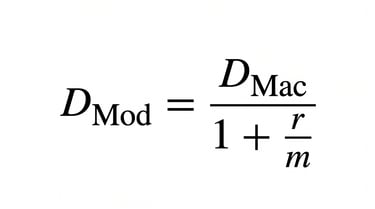

To accurately measure and manage this interest rate risk, corporate finance teams calculate Macaulay Duration and Modified Duration. Macaulay Duration computes the weighted-average time an investor must wait to receive all cash flows from a bond, measured in years:

Modified Duration converts this timeframe into a direct measure of price volatility, showing the exact percentage change in a bond's price for a 1% change in market interest rates:

Where m is the number of compounding periods per year. If a corporate bond has a Modified Duration of 7.5, a 100-basis-point (1%) increase in market interest rates will cause an immediate 7.5% drop in the bond's market price.

4. Deconstructing the Yield Matrix: Cost of Capital Mechanics

When evaluating debt issuances or portfolio assets, financial executives look beyond standard pricing to analyze the underlying yields that dictate capital efficiency:

Current Yield: Measures the annual cash return generated by the bond relative to its current market price (Current Yield = Annual Coupon Payment / Current Market Price). This metric is useful for tracking short-term income production, but it ignores capital gains or losses realized at maturity.

Yield to Maturity (YTM): The internal rate of return (IRR) earned by an investor who buys the bond at its current market price and holds it until maturity. YTM assumes all intermediate coupon payments are reinvested at that same rate, making it the benchmark metric for corporate cost-of-debt calculations.

Yield to Call (YTC): Essential for evaluating callable bonds, which grant corporate issuers the legal right to repurchase debt before its scheduled maturity. If market interest rates drop, corporate treasurers will call back high-interest bonds and refinance at a lower cost, truncating investor returns.

By monitoring how these risk premiums fluctuate in the open market, future corporate executives can accurately gauge consumer confidence, evaluate changing macroeconomic risks, and strategically time debt issuances to capture the lowest possible cost of capital.

Contact

Questions? Reach out anytime.

© 2025 BizSphere. All rights reserved.